Workflow

Input to output

in four automated steps

Step 01 - Security Entry

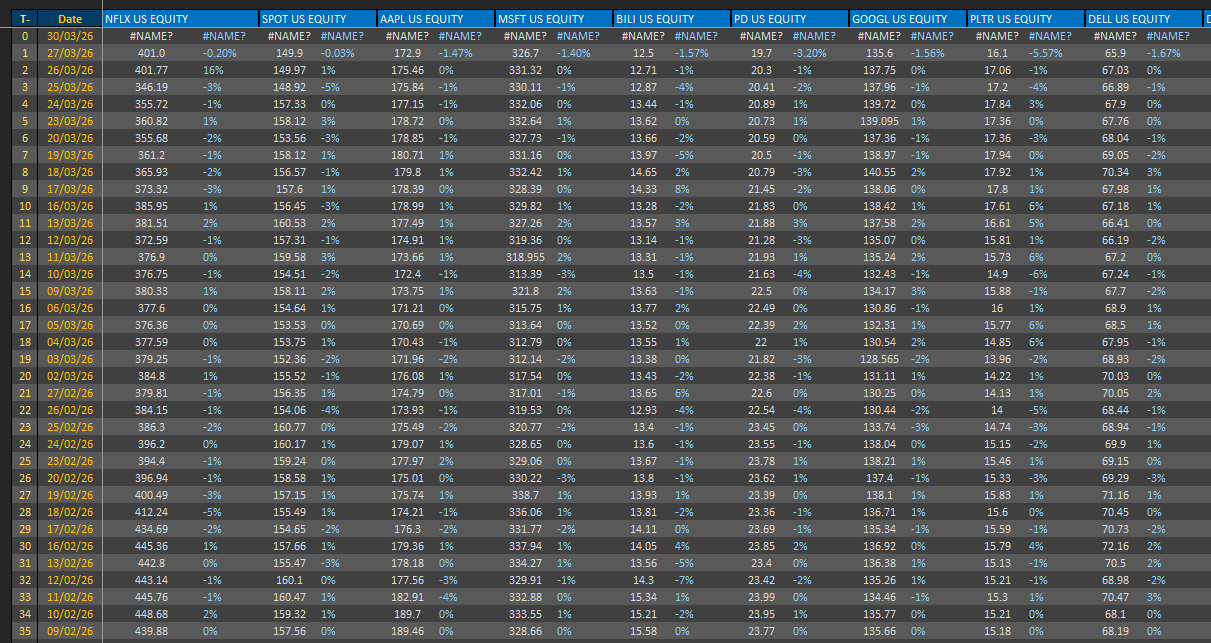

Define the universe

Enter Bloomberg tickers for up to 30 equities. The sheet uses BDP and BDH functions to auto-populate security names, live market capitalisations, and YTD performance in real time.

Step 02 - Price Data

Pull 3 years of history

Bloomberg fetches daily closing prices for each security going back 750 trading days. Daily returns are calculated alongside - these are the raw inputs that feed every downstream calculation.

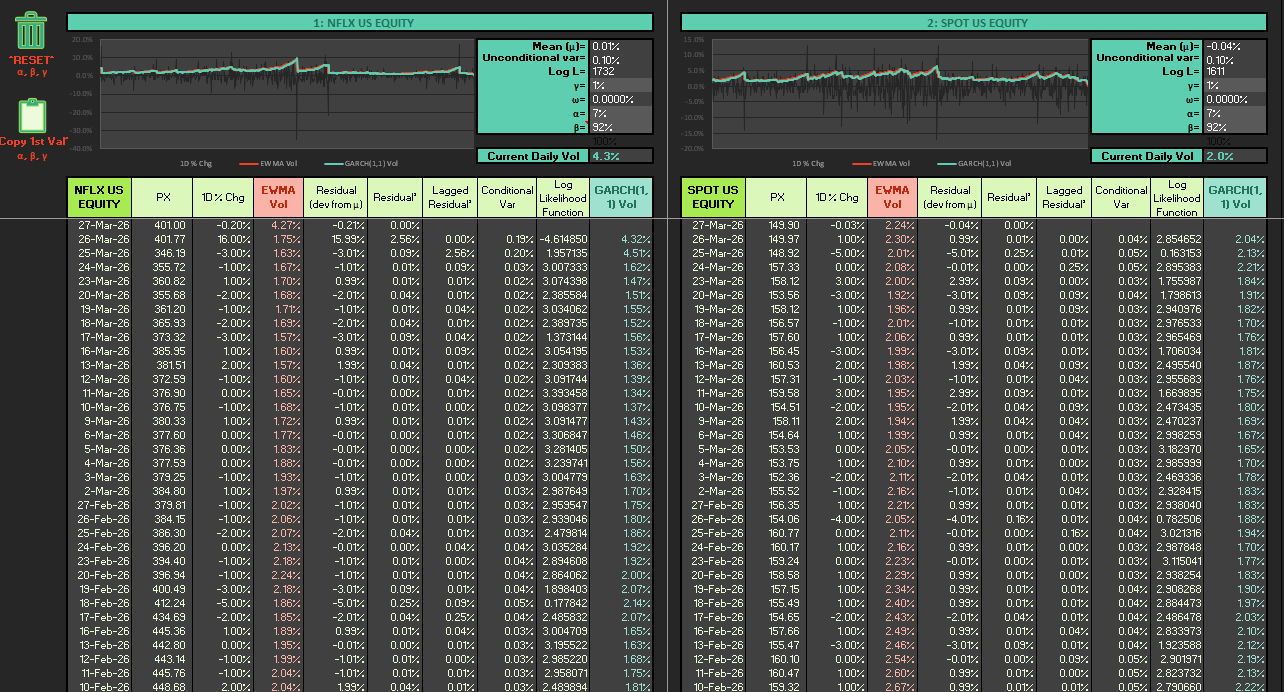

Step 03 - GARCH Volatility

Estimate dynamic volatility

A GJR-GARCH(1,1) model estimates conditional volatility for each security using 3 years of daily returns. Parameters α, β, and γ are optimised per asset by maximising the log-likelihood function via the Excel Solver.

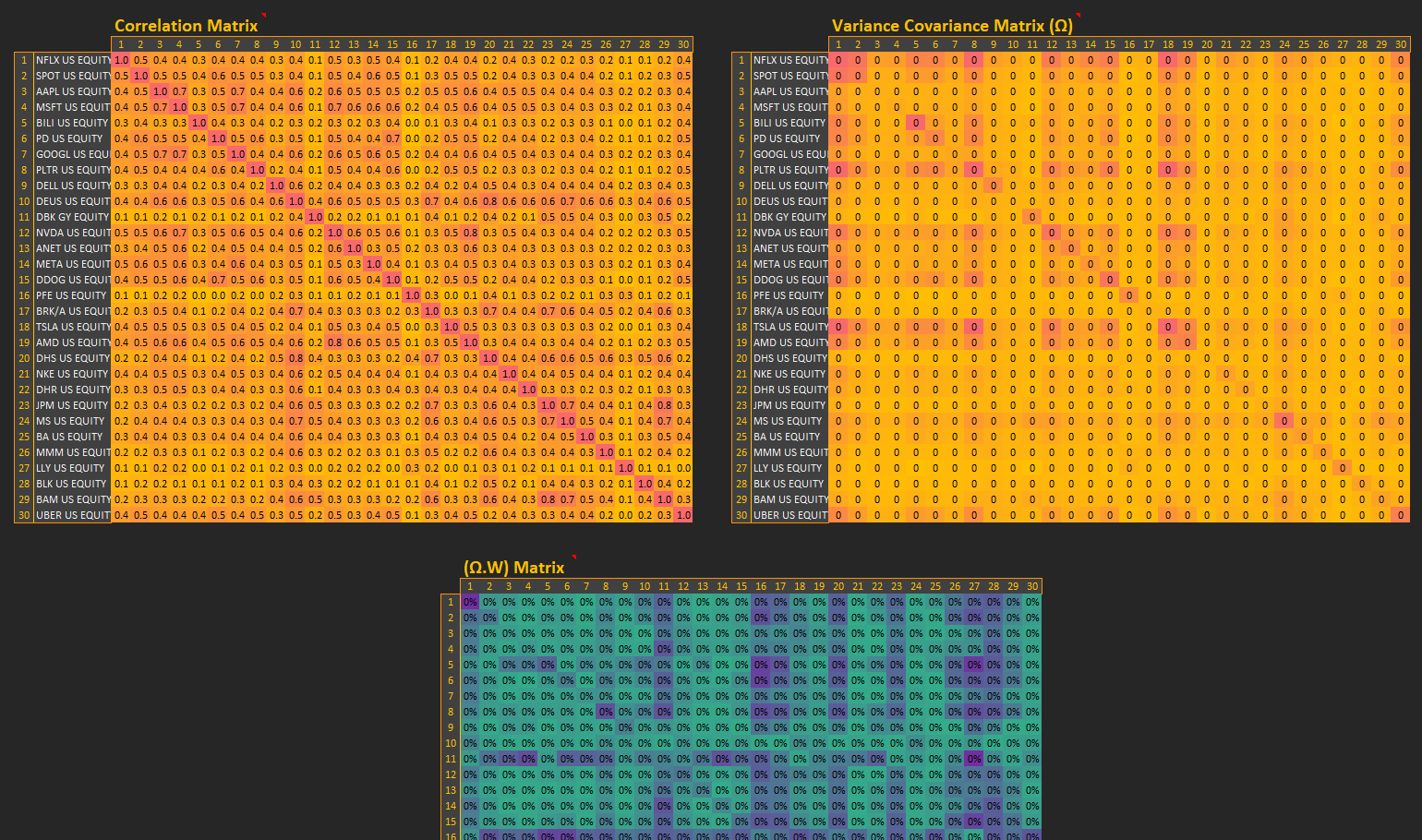

Step 04 - Matrix Construction

Build the covariance structure

Three matrices are computed: the correlation matrix, the variance-covariance matrix (Ω), and the Ω × Weights matrix. All are dynamically linked and update whenever the allocation method or underlying weights change.

Step 05 - Portfolio Output

Optimised weights, instantly

Select the desired method from the DistMeth dropdown. EW and IV weights recalculate instantly. ERC and MinVol trigger standalone Python solvers - bundled as compiled executables, so no Python install is needed on the recipient machine.