Workflow

From one company

to a price target

Step 01 — P&L Engine

Build the financial spine

Enter the company's income statement by hand — seven years of history from revenue through diluted EPS, split into annual and quarterly columns with automatic period headers, margin lines, and YoY growth. Only the forward/estimate columns are wired to Bloomberg consensus; everything historical is manual input. Every downstream method reads from this sheet.

Step 02 — DCF

Value the cash flows

FCF is projected from forecast revenue growth, operating margin, tax, D&A, capex, and working capital. The discount rate is a full WACC — cost of equity via CAPM (risk-free, equity risk premium, Bloomberg beta) and after-tax cost of debt, weighted by capital structure. Terminal value uses the Gordon growth approach. Output is intrinsic equity value per share and upside to market.

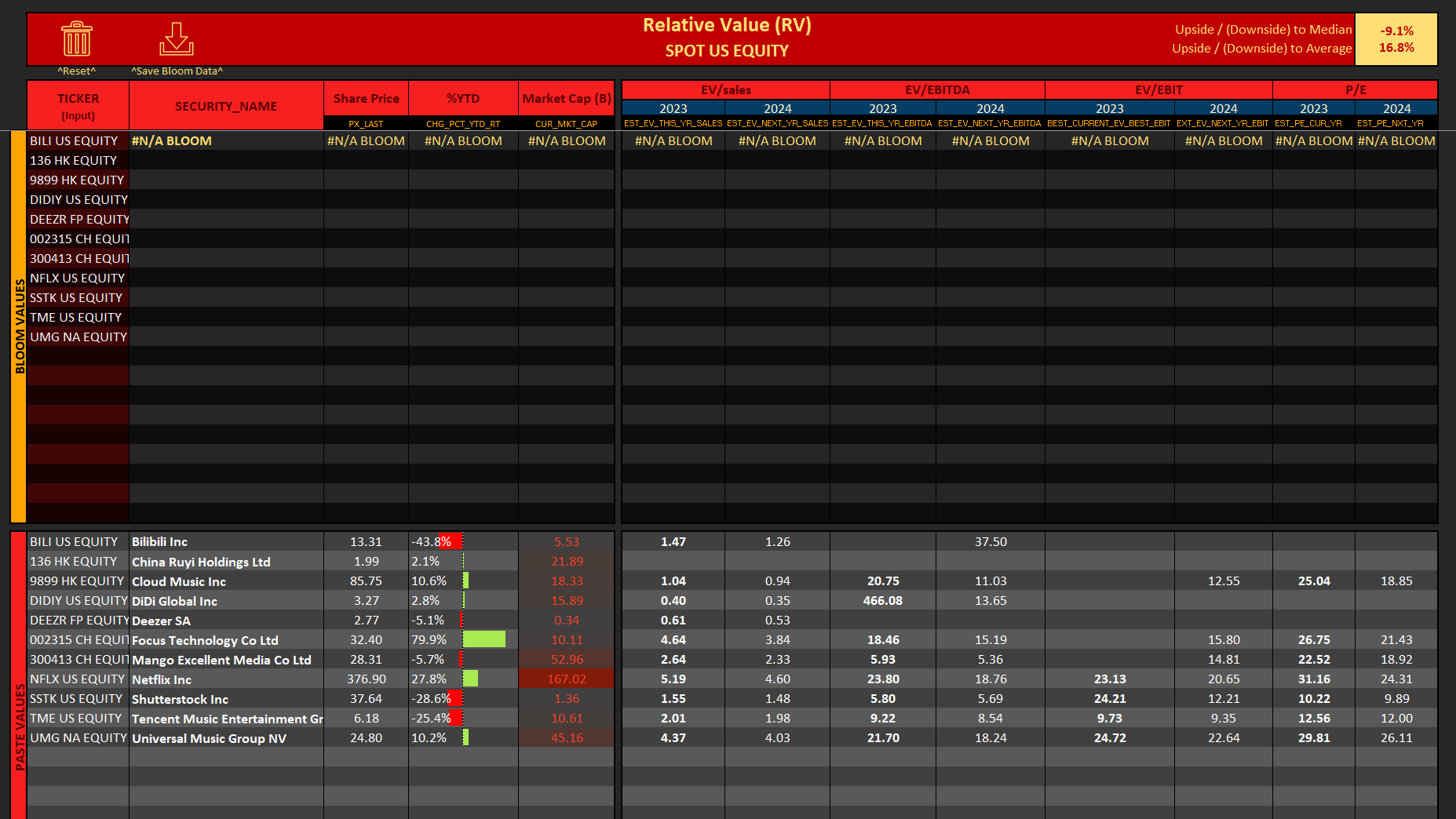

Step 03 — Relative Value

Benchmark the peers

Build a comparable set by ticker. Bloomberg populates names, prices, market caps, and EV multiples (EV/Sales, EV/EBITDA, EV/EBIT) on current and forward years. The model computes peer average and median, then the target's implied upside or downside to each.

Step 04 — Sum of the Parts

Break it up

Value each operating division (EV/Sales, EV/EBITDA, or EV/NOPAT) and each minority stake on a DCF or NAV basis. Net debt and other liabilities are subtracted, a holdco discount applied, and the result divided by shares outstanding for an SOTP value per share.

Step 05 — Final Blend

One number

The three methods feed a weighting table — set any split across DCF, RV, and SOTP. The sheet returns the blended equity value per share and total upside against the live price.